How India's CFCFRMS (1930) and the FBI's Recovery Asset Team handle online financial crimes

A step-by-step comparison of the financial-fraud interception machinery of the world's largest digital-payments market and the world's largest economy

21st May, 2026, New Delhi

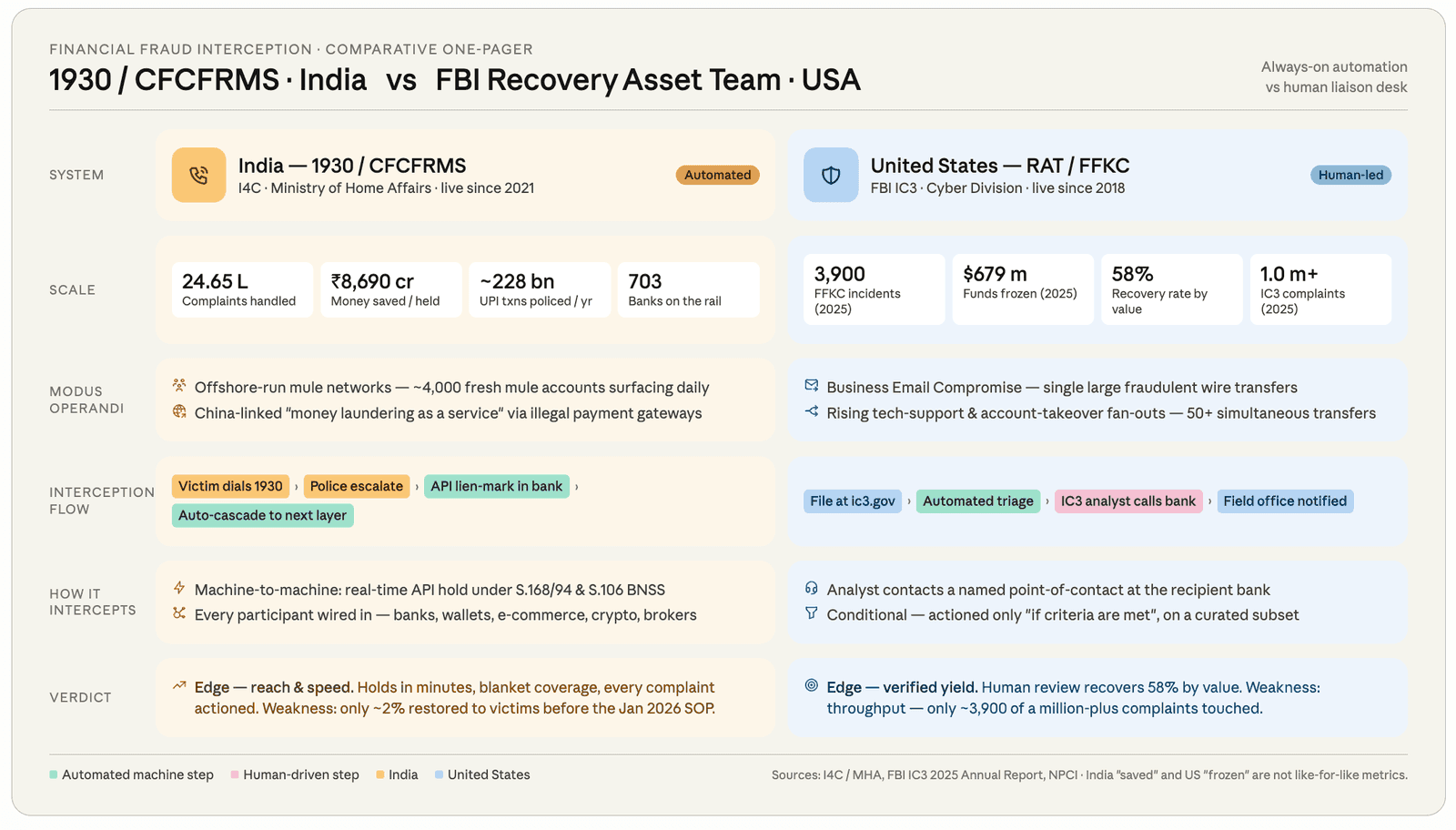

When a victim of online fraud in Mumbai dials 1930, and when a victim in Miami files a complaint at ic3.gov, each has triggered a race. On one side is a criminal moving stolen money through a chain of accounts; on the other is a system trying to freeze that money before it disappears. India and the United States have each built such a system. They were designed for very different financial ecosystems, and they work in very different ways. This is a structured comparison of the two, India's Citizen Financial Cyber Fraud Reporting and Management System (CFCFRMS), run by the Indian Cyber Crime Coordination Centre (I4C), and the Recovery Asset Team (RAT) of the FBI's Internet Crime Complaint Center (IC3), which operates the Financial Fraud Kill Chain (FFKC).

The headline difference can be stated up front. India has built an always-on, machine-to-machine settlement-layer intervention. The United States operates a human-coordinated liaison desk. Both are effective at what they were built for.

1. The scale of the problem each system was built to solve

The two systems were not built to the same specification because the threat is not the same size.

The United States, despite being a larger economy, reports a more concentrated fraud problem in volume terms. IC3 recorded 1,008,597 complaints in 2025, with reported losses of $20.877 billion, of which roughly 85%, about $17.7 billion, was cyber-enabled fraud. Of that universe, the Recovery Asset Team's Financial Fraud Kill Chain was actually triggered on only 3,900 incidents in 2025.

India's CFCFRMS operates at a categorically different transaction volume. The system has handled more than 24.65 lakh (2.465 million) complaints through to 31 January 2026, and the underlying flow it polices is enormous: India's Unified Payments Interface alone processed roughly 228 billion transactions worth nearly ₹300 lakh crore in calendar year 2025, averaging close to 700 million transactions a day. A single national interception system in India is therefore sitting on top of the largest real-time retail-payments rail in the world.

The implication is structural. A liaison-desk model that processes a few thousand cases a year cannot be transplanted onto a payments system clearing hundreds of millions of transactions daily. India's choice of an API-driven, automated architecture is not a matter of ambition; it is a matter of necessity.

| Dimension | India, CFCFRMS (I4C) | United States, RAT/FFKC (FBI IC3) |

|---|---|---|

| Operational since | April 2021 | February 2018 |

| Total complaints handled | 24.65 lakh+ (to 31 Jan 2026) | 1,008,597 IC3 complaints in 2025 alone |

| Interception events | Essentially every escalated CEFC complaint | 3,900 FFKC incidents initiated (2025) |

| Underlying payments rail | ~228 bn UPI transactions/year (CY2025) | ACH / wire / card rails |

| Money saved / frozen | ₹8,690 crore saved (to 31 Jan 2026) | $679 million frozen (2025) |

One of the major differences in India and USA's financial space is Real Time Transactions or Instant Payments. India handles 50% of Global real time payments in the world, which requires a system which can stop the money in real time.

Key Comparison Metrics (Latest Available Official/near-Official Data, as of early-mid 2026)

| Metric | India (UPI - NPCI) | USA (FedNow + RTP) | Notes |

|---|---|---|---|

| Monthly Volume | ~20-22+ billion transactions (e.g. March 2026: 22.6 billion) | FedNow: ~2.7 million (Q1 2026); RTP: ~100-128 million (e.g. Q1 2026: 128 million) | UPI processes ~100-200x more transactions monthly. India handles ~50% of global real-time payment volume. |

| Monthly Value | ~₹25-30 lakh crore (~$290-350+ billion USD) (e.g. March 2026: ₹29.5 lakh crore) | FedNow: ~$271 billion (Q1 2026); RTP: ~$480 billion (Q1 2026) | Combined US ~$700+ billion possible in peak quarters, but UPI value is comparable or higher at retail scale. |

The world is moving towards instant settlement and fast payments, which makes it imperative for fraud management and reporting system to catch up with faster withdrawals.

2. Ease of Reporting: how a victim reports to Government

| India, CFCFRMS | United States, RAT/FFKC | |

|---|---|---|

| Primary channels | Helpline 1930 (voice), cybercrime.gov.in portal, any police station, and registration by banks on the victim's behalf | ic3.gov complaint portal; victim is also urged to call their own bank directly |

| Channel design | Multi-modal, including a 24x7 voice line operated by State police | Single web intake; no dedicated national fraud-recall hotline |

| Speed expectation | "Golden hour" reporting explicitly designed in | "Time is of the essence", IC3 urges filing "as quickly as possible" |

| Acknowledgement | 14-digit acknowledgement number issued by SMS | Complaint ID issued on filing |

India's reporting layer is deliberately broader. The 1930 voice helpline matters in a country where a fraud victim may not be comfortable navigating a web form, and the explicit "report within the golden hour" messaging, reinforced through caller-tune campaigns, IPL advertising and campaigns at the Kumbh Mela, treats speed of citizen reporting as a public-awareness target in itself.

The US model places more of the initial burden on the victim to also contact their own financial institution to request a recall and obtain a "Hold Harmless Letter" or "Letter of Indemnity." IC3's guidance is candid that "different financial institutions have varying policies", an admission that, in the US, the first and fastest line of defence is the bank's own recall process, not the federal system.

Verdict on ease of reporting: India's system is more accessible to the ordinary citizen, principally because of the 1930 voice channel and the ability of banks and police stations to file on a victim's behalf.

3. The interception engine: API automation versus human liaison

This is the heart of the comparison, and the sharpest divergence.

India: a settlement-layer API integration

When a complaint is escalated to CFCFRMS, the system does not primarily route a human request to a human contact. It pushes a legally-backed electronic notice, under Section 168 read with Section 94 of the Bharatiya Nagarik Suraksha Sanhita (BNSS) for holds, and Section 106 BNSS for seizures, directly into the banking system. Crucially, API integration between banks and the CFCFRMS module has been implemented, enabling, in I4C's own description, "real-time communication and exchange of information, data updation and consequent action of lien marking."

The practical consequence is that a beneficiary bank can place a hold on the suspect amount and update the money trail back onto the portal as a machine transaction. Where funds have already moved on, the receiving bank updates the exit details, and the notice cascades to the next institution in the chain. The system is designed to chase money across layers automatically until the trail ends.

This automation extends across an unusually wide set of participants. The CFCFRMS Standard Operating Procedure issued on 2 January 2026 prescribes specific interception duties not just for banks but for e-commerce companies, Payment System Operators, PPI/wallet and CBDC issuers, Payment Aggregators and Gateways, Business Correspondents, cross-border remittance firms, credit-card issuers and acquirers, mutual fund and stock-broking companies, and Virtual Asset Service Providers (crypto exchanges), the last required to liquidate crypto into rupees and route it back to the victim.

United States: a triage-and-liaison desk

The RAT process, as the FBI's own Domestic Financial Fraud Kill Chain diagram sets out, runs as a sequence of discrete steps: Victim → IC3 complaint → System Automated Triage → IC3 Database → IC3 Analyst review → contact with the Financial Institution's identified point of contact → response received → RAT notifies the relevant FBI Field Office.

Two features stand out. First, only the triage is automated; the decisive interception step is an IC3 analyst contacting a named point-of-contact at the recipient bank. Second, the FFKC is conditional, the FBI's documentation states that "if criteria are met," transaction details are forwarded to the bank. There is a threshold; not every complaint is actioned.

The strength of the US model is that human review reduces false positives and the FFKC has, since 2025, been explicitly extended to chase the "second hop", funds that have moved beyond the first recipient bank, including to international accounts via coordination with FinCEN's Rapid Response Team. The weakness is throughput: a liaison desk is inherently rate-limited by analyst capacity, which is consistent with the FFKC being triggered on only 3,900 of more than a million complaints.

| Interception attribute | India, CFCFRMS | United States, RAT/FFKC |

|---|---|---|

| Core mechanism | Machine-to-machine API notice into banks | IC3 analyst phones/emails a bank point-of-contact |

| Automation depth | End-to-end: hold, lien marking, trail update | Triage only; intervention is human |

| Coverage | Every escalated cyber-enabled financial crime | Conditional, "if criteria are met" |

| Legal instrument | Statutory notice (S.168/94, S.106 BNSS) | Request to bank; relies on bank recall policy + indemnity |

| Layer-chasing | Automatic cascade to next institution | "Second hop" pursued, analyst-driven |

4. Speed of tracing

Speed is where the architectural choice pays off, or doesn't.

India's API model is, in principle, capable of placing a hold within minutes of escalation, because lien marking is a system action rather than a phone call. The SOP's design intent is real-time: it explicitly requires "Participating Entities to take real-time action to put on hold a reported transaction."

The US model's speed is bounded by business hours and human availability. The instructive external benchmark cited in India's own SOP is the US Bank Secrecy Act framework, under which banks can freeze suspicious accounts "often within 24–48 hours of detection", a useful yardstick, but an order of magnitude slower than a real-time API hold.

That said, raw speed is not the only measure. The US recovery rate is high precisely because human analysts pre-qualify cases. In 2025 the FFKC achieved a 58% success rate by value ($679 million frozen against $1.164 billion in attempted theft). India's saved figure, ₹8,690 crore, is large in absolute terms, but it is a small fraction of the total reported fraud (the SOP records ₹7,647 crore prevented against ₹52,969 crore reported between April 2021 and November 2025, roughly 14%).

The speed-versus-yield trade-off is the single clearest distinction between the two systems. India optimises for speed and reach; the US optimises for verified yield on a curated subset.

5. Layering-detection and money-trail intelligence

Modern fraud is defeated less by catching the first transfer than by reading the chain. Here both systems have invested, but differently.

India has built a data-and-analytics estate around CFCFRMS that goes well beyond interception:

- A Suspect Registry of cyber-criminal identifiers, launched September 2024, which by 31 January 2026 had ingested 23.05 lakh suspect identifiers from banks and shared 27.37 lakh "Layer-1" mule accounts with participating entities, directly declining transactions worth ₹9,518.91 crore.

- The Samanvaya platform, an MIS and data repository providing analytics-based interstate linkage of crimes and criminals, and its Pratibimb module, which maps criminal infrastructure geographically; together credited with over 21,857 arrests.

- A new I4C–Reserve Bank Innovation Hub partnership and AI tooling (MuleHunter.ai) aimed specifically at detecting hidden mule accounts.

- A Cyber Fraud Mitigation Centre (CFMC) physically co-locating major banks, intermediaries, payment aggregators, telecom operators and State police for joint action.

The explicit target of all this is layer detection, the SOP's worked illustrations show, in granular detail, how holds are marked across "first-layer" mule accounts and how commingled funds are attributed.

The US RAT, by contrast, is principally an interception and statistics function. The FBI states the RAT's goals are to "assist in the identification of potentially fraudulent accounts" and to "remain at the forefront of emerging trends." Layering analysis in the US is real but is distributed across other bodies, FinCEN, the banks' own AML systems, and FBI field investigations, rather than concentrated in the RAT itself.

Verdict on layering detection: India has built a more centralised, purpose-specific layering-detection apparatus, driven by the mule-network nature of its threat.

6. Participants on the system: who is plugged in

The breadth of mandatory participation is one of CFCFRMS's defining features.

India, CFCFRMS stakeholders (per the SOP) include: all categories of banks (public, private, cooperative, small finance, payments, regional rural and local area banks); the RBI, NPCI, SEBI, IRDAI, NABARD, PFRDA and the Department of Financial Services; the Indian Banks' Association; e-commerce platforms; NBFCs, payment aggregators, gateways, business correspondents and loan service providers; insurance companies; stock exchanges, mutual funds and broking companies; virtual asset / cryptocurrency exchanges; and the police of every State and Union Territory.

This is an unusually wide net. It means a fraud that exits through a crypto exchange, a gift-card purchase, an e-commerce coupon, a mutual-fund trade or a cross-border remittance still lands on the same portal, and BSE's notice of 23 March 2026, drawing trading members' attention to Para 9.6 of the SOP, shows the securities industry being formally folded in.

United States, RAT/FFKC participants centre on the financial institutions that maintain a point-of-contact relationship with the IC3, the IC3 itself, FBI field offices, and, for international cases, FinCEN's Rapid Response Team, FBI LEGAT offices and foreign law-enforcement partners. It is a tighter, law-enforcement-centric network. The FBI describes the goal as a "symbiotic relationship in which information is appropriately shared" between law enforcement and banks, a partnership model rather than a regulatory-mandate model.

7. The institutional terrain: how many banks must be wired in

The two systems must integrate with banking sectors of very different shape.

India must reach an exceptionally fragmented system. As of 1 August 2025 India had 128 commercial banks (124 scheduled), 12 public sector, 21 private, 28 regional rural, 44 foreign, 12 small finance, 6 payments and 2 local area banks, plus a long cooperative tail, including roughly 1,457 urban cooperative banks. By a different and revealing measure, 703 banks are live on the UPI rail. Wiring an API-based interception system into a sector this fragmented is a formidable integration task, and the SOP openly states that "onboarding of remaining stakeholders is ongoing."

The United States has an even larger number of chartered banks and credit unions in absolute terms, several thousand, but the RAT does not need to API-integrate with all of them. Because the model is a liaison desk, the RAT only needs a point-of-contact relationship with the institutions where fraud proceeds tend to land. A human-liaison model scales differently from an API model: it does not require universal technical onboarding, but it cannot act on an institution with which no contact has been pre-established.

This is a genuine trade-off, not a clear win for either side. India's universal-API ambition delivers blanket coverage but demands enormous integration effort across a fragmented sector. The US liaison model sidesteps the integration problem but accepts narrower, relationship-dependent reach.

8. Ease of victim recovery: getting the money back

Freezing money and returning it are two different problems, and both systems are visibly weaker at the second.

India's most striking admission is in the SOP itself: of the money saved, only ₹167 crore, about 2.18%, had actually been restored to victims at the time of drafting. The 2 January 2026 SOP exists precisely to fix this. It introduces five alternative legal routes for interim custody and restoration, including a fast track under Section 106(3) BNSS for single victims, a structured pro-rata distribution process where mule-account funds are commingled across multiple victims, and disposal through the courts under Sections 497, 498, 503 and 107 BNSS, plus a dedicated Money Restoration Module and a time-bound Grievance Redressal Mechanism (with 7-day, 15-day and 90-day clocks and a tiered District/State grievance-officer appeal structure).

The US model folds recovery into the freeze: once funds are frozen at the recipient bank, return to the victim proceeds through the bank's recall process and the indemnification documents the victim was advised to obtain, with FBI field offices and the courts handling contested or criminal cases. It is less elaborate on paper than India's new five-process framework, but it also serves a far smaller caseload.

Both countries' frameworks now converge on a principle India's SOP documents at length from global precedent: where victims' funds are commingled and cannot be individually traced, pro-rata distribution by verified loss is the accepted fair method, the approach used in the Madoff and NSEL/63 Moons recoveries alike.

Conclusion: not better or worse, but built for different battles

The two systems are rational answers to different questions.

The FBI's Recovery Asset Team is a precision instrument: human-curated, high-yield, conservative in what it actions, and effective at recovering large sums in a fraud landscape still anchored by big-ticket BEC wires. Its limitation is throughput, it cannot, and does not try to, touch most complaints.

India's CFCFRMS is an industrial-scale interception machine, possibly one of largest in the world, built to cater a payments rail clearing 700 million transactions a day, attacked by offshore-run mule networks generating thousands of fresh mule accounts daily, cannot be defended by a liaison desk. Its API-driven, all-participants, real-time design is the more ambitious architecture, and the more necessary one.

The honest bottom line is that India has built the more scalable model and the United States the more consistently effective per-case model. If India's new SOP succeeds in lifting restoration from 2% toward something closer to the FFKC's 58% yield, it will have combined the reach of an automated system with the recovery discipline of a curated one. That, not a choice between the two philosophies, is the benchmark worth watching.